Discretionary spending refers to non-essential costs that you can skip without disrupting your daily life or survival. Often labeled as "wants" rather than "needs," discretionary expenses come from your discretionary income — the money left over after covering necessities like rent, groceries, and taxes.

In this article, you'll learn:

- Key characteristics that define discretionary expenses

- Budgeting strategies to manage spending wisely

- How discretionary costs compare to mandatory and fixed expenses

- Common examples of discretionary spending for individuals and businesses

Understanding where your money goes — and why — puts you in control of your financial future.

What Are the Key Characteristics of Discretionary Spending?

Discretionary expenses share several traits that distinguish them from essential costs. Recognizing these characteristics helps you identify which expenses to cut first when money gets tight.

Financial Flexibility

The defining feature of discretionary spending is flexibility. You can reduce or eliminate these costs without serious consequences to your well-being or operations. When economic conditions worsen, or unexpected bills arrive, discretionary items become the first candidates for cuts — precisely because removing them won't derail your life.

Discretionary expenses get funded only after mandatory costs are covered. Your rent, utilities, and minimum debt payments take priority. Whatever remains becomes your discretionary pool for entertainment, dining out, and other lifestyle choices.

Price Sensitivity

In economic terms, discretionary items are considered price elastic. When prices rise, people quickly reduce purchases of non-essential goods.

| Expense Type | Price Sensitivity | Cutting Impact |

|---|---|---|

| Discretionary | High (elastic) | Minimal lifestyle disruption |

| Non-discretionary | Low (inelastic) | Serious consequences |

A 20% increase in concert ticket prices might prompt you to attend fewer shows, but a similar increase in electricity rates won't stop you from keeping the lights on.

Subjectivity and Context

What counts as discretionary varies considerably between people. A gym membership might be a luxury for someone with a home workout routine, yet essential for a personal trainer. Similarly, a car represents a discretionary purchase for city dwellers with public transit access — but becomes mandatory for rural commuters with no alternatives.

The same logic applies to businesses. An internet connection is non-negotiable for a cloud storage company, however, a small retail shop might function without it — making connectivity discretionary in that context.

What Are Examples of Discretionary Expenses?

Discretionary spending looks different depending on whether you're managing a household budget or running a business. The common thread is that these costs support lifestyle or growth rather than basic survival.

Personal Expenses

Individual discretionary spending typically falls into lifestyle and entertainment categories:

- Vacations and leisure travel

- Gifts and charitable donations

- Luxury goods and designer items

- Gym memberships and hobby supplies

- Streaming subscriptions and cable packages

- Concert tickets and movie outings

- Dining out and restaurant meals

- Specialty coffee and alcohol

Business Expenses

Companies also carry discretionary costs — often tied to growth initiatives or employee satisfaction rather than daily operations:

- Merger and acquisition activity

- Office renovations and upgrades

- Research and development projects

- Marketing and advertising campaigns

- Employee perks and training programs

Context Matters

Some expenses shift categories based on circumstances. Upgrading to the latest smartphone when your current device works fine is clearly discretionary. However, replacing a broken phone that you need for work becomes mandatory.

A startup might consider advertising essential for building exposure, while an established company could temporarily cut that same budget during a downturn.

How Does Discretionary Spending Compare to Other Expenses?

Understanding the distinction between expense categories helps you prioritize during budgeting and make smarter trade-offs when income fluctuates.

Mandatory Expenses

Non-discretionary (or mandatory) expenses are costs you must pay to maintain basic living standards. Missing these payments triggers real consequences — eviction, utility shutoffs, or legal action.

Common mandatory expenses include:

- Housing costs (rent or mortgage)

- Utilities (electricity, water, heat)

- Groceries and essential food

- Minimum debt payments

- Insurance premiums

- Taxes

When income drops, mandatory expenses remain relatively stable. You might negotiate payment plans, but you can't simply skip them the way you'd cancel a streaming subscription.

Fixed Expenses

Fixed expenses are predictable costs that recur at regular intervals. Rent, insurance premiums, and loan payments fall into this category. Most fixed expenses also qualify as mandatory — though not always. A monthly magazine subscription is fixed (same amount each month) but entirely discretionary.

Key Differences

| Factor | Discretionary | Mandatory | Fixed |

|---|---|---|---|

| Necessity | Low | High | Varies |

| Flexibility | High | Low | Low |

| Cutting consequences | Minor | Severe | Depends on type |

| Examples | Entertainment, travel | Rent, utilities | Rent, subscriptions |

What Budgeting Strategies Help Manage Discretionary Spending?

Managing discretionary expenses effectively requires intentional planning. Several proven approaches can help you balance enjoying life today with building financial security for tomorrow.

Tracking and Identification

The first step involves separating discretionary costs from essential ones. Review your bank statements and categorize each expense. Seeing exactly where money flows reveals surprising patterns — that daily coffee habit adds up faster than you'd expect.

Prioritization

Once you've identified discretionary expenses, rank them from least to most important. When budget cuts become necessary — due to job loss or unexpected bills — this ranking tells you exactly where to start trimming. Most people would rather keep internet service than cable television, for instance.

Budgeting Methods

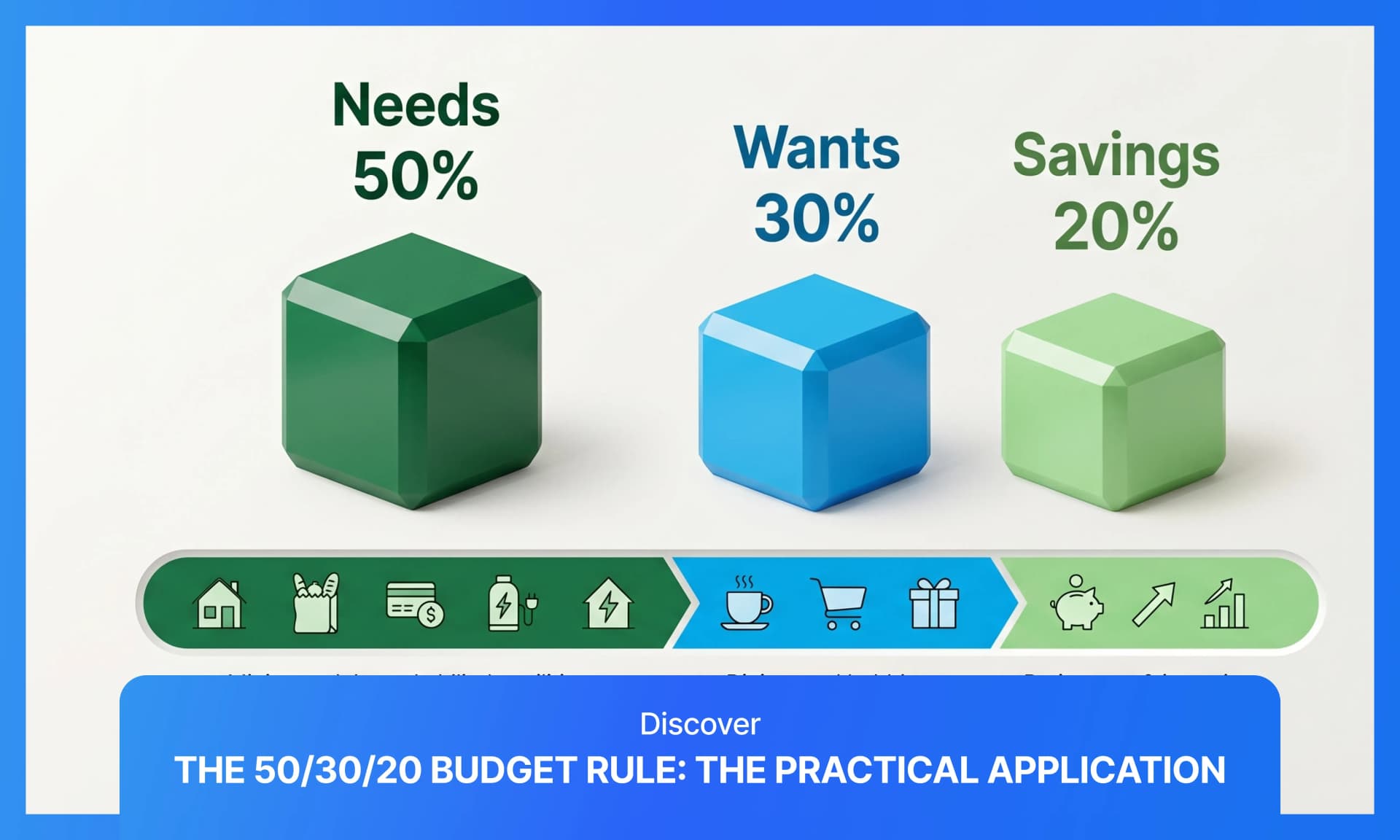

Several popular frameworks allocate specific percentages to discretionary spending:

| Method | Needs | Savings/Debt | Discretionary |

|---|---|---|---|

| 50/30/20 rule | 50% | 20% | 30% |

| 50/15/5 approach | 50% | 20% (15% retirement + 5% short-term) | 30% |

| Zero-based budgeting | Assigned | Assigned | Assigned |

The 50/30/20 rule offers simplicity — allocate half your take-home pay to needs, 20% to savings or debt repayment, and 30% to wants. Zero-based budgeting takes a different approach by assigning every dollar a specific purpose before the month begins.

Trade-Offs

Effective budgeting often involves trade-offs rather than outright elimination. Someone who values live music might cancel a cable package — switching to cheaper streaming — to free up concert funds. The goal isn't deprivation; it's aligning spending with what actually matters to you.

Transparent Transfers Maximize Your Discretionary Income

Every dollar lost to hidden fees or poor exchange rates reduces the discretionary income available for things you care about. When sending money internationally, choosing a provider with transparent pricing keeps more money in your pocket.

RemitBee helps Canadians stretch their discretionary budgets further:

- Zero fees on transfers over $500 CAD

- Transparent FX rates without hidden markups

- FINTRAC regulated for security and compliance

- Multiple payment options, including Interac e-Transfer and EFT

Start saving on your next international transfer with RemitBee.

References

- Investopedia. Discretionary Expense Definition.

- Congressional Budget Office. Discretionary Spending Reports.

- U.S. Government Accountability Office. Federal Budget Structure Overview.

Frequently Asked Questions

Is Sending Money Abroad a Discretionary Expense?

It depends on the purpose. Supporting family members who rely on your remittances for basic needs makes the transfer mandatory. Sending gift money for celebrations or special occasions typically falls into discretionary territory.

How Much of My Income Should Go to Discretionary Spending?

Most budgeting frameworks recommend keeping discretionary spending at or below 30% of your take-home pay. However, the right percentage depends on your financial goals, debt levels, and cost of living in your area.

Can Discretionary Expenses Become Non-Discretionary?

Absolutely. Circumstances change what's essential. A car becomes mandatory when you accept a job requiring a commute. An internet connection shifts from optional to necessary when you start working remotely.

How Do Economic Recessions Affect Discretionary Spending?

During recessions, discretionary spending typically drops significantly. Consumers and businesses cut non-essential costs first to preserve cash flow. Companies selling luxury goods or entertainment services often experience sharp revenue declines during economic downturns.

Are Subscription Services Discretionary or Essential?

Most subscriptions qualify as discretionary — streaming services, gym memberships, and magazine subscriptions can all be canceled without serious consequences. However, software subscriptions required for work or essential communication tools might be mandatory depending on your situation.