You've probably felt that sinking feeling when you check your bank account mid-month and wonder where all your money went. You earned it, you spent it, but somehow the important things (like sending money home or building an emergency fund) got pushed aside again.

What is zero-based budgeting?

Zero-based budgeting means assigning every dollar of your income to a specific category until you reach zero. The "zero" doesn't mean having nothing left (that would be terrifying). Instead, it means your income minus all your planned expenses, savings, and goals equals zero.

Think of it like this: you're the manager of your money, and every dollar is an employee. Nobody gets to just hang around doing nothing. Each one receives an assignment, whether that's paying rent, buying groceries, going into savings, or funding their monthly transfer to family back home.

Zero-based budgeting was developed by Peter A. Pyhrr at Texas Instruments in the late 1960s and introduced to the public in his 1970 Harvard Business Review article. President Jimmy Carter later adopted it in government budgeting in Georgia before mandating it across US federal agencies in 1977, asking departments to justify every expense from scratch rather than just adjusting previous budgets.

Personal finance experts adapted this corporate and government approach because it creates the same discipline for household finances. When you must account for every dollar, waste becomes obvious and priorities get clearer.

How does zero-based budgeting work?

The process sounds intensive, but it becomes second nature after a few months. You'll create a spending plan that accounts for your entire income before the month starts.

Calculate your monthly income

Start with your actual take-home pay after taxes, insurance, and other deductions. If you're paid bi-weekly, figure out which months have three paychecks (bonus months that deserve special planning).

For variable income situations (like commission-based work or freelancing), use your lowest typical month as the baseline. You can always allocate extra money when you earn more, but planning for the minimum keeps you safe.

List all your expenses

You'll need to capture everything you spend money on throughout the month.

- Fixed expenses

- Your fixed costs stay relatively consistent:

- Subscription services

- Phone and internet bills

- Rent or mortgage payments

- Regular international money transfers

- Insurance premiums (health, auto, renters)

- Loan payments (student loans, car payments)

Variable expenses

Variable costs fluctuate, but still need planning:

- Utilities (electricity, water fluctuate seasonally)

- Transportation (gas, public transit)

- Groceries and household supplies

- Entertainment and dining out

- Personal care and clothing

- Medical expenses

- Savings and debt payments

Budget these categories just like bills:

- Retirement savings

- Emergency fund contributions

- Sinking funds for irregular expenses

- Extra debt payments beyond minimums

- Specific savings goals (vacation, car down payment)

Sinking funds deserve a quick explanation because they're budget-savers. You set aside money each month for expenses that hit annually or irregularly (like car registration, holiday gifts, or insurance premiums). When the bill arrives, the money is already waiting.

Assign every dollar a job

Take your total monthly income and start allocating it to each category you listed. Keep going until you've assigned every single dollar.

Your math should look like: Income - (All expenses + Savings + Debt payments) = $0

If you end up with money left over after covering everything, don't leave it unassigned. Put it somewhere intentional (extra savings, additional debt payment, or a fun money category). If your expenses exceed your income, you'll need to make cuts by examining variable expenses first.

Track and adjust throughout the month

Creating the budget is half the work. You also need to track your actual spending against your plan as the month progresses.

When you overspend in one category, you must pull money from another to cover it. Let's say you budgeted $400 for groceries but spent $450. You need to reduce another category by $50 to balance things out (maybe from dining out or entertainment).

This mid-month adjustment makes zero-based budgeting powerful. You're constantly aware of trade-offs and making conscious choices about priorities.

What are the benefits of zero-based budgeting?

The advantages go beyond just knowing where your money goes (though that alone is valuable).

Awareness

You gain complete awareness of your financial situation. There's no mystery about why your account is low or where that $200 disappeared. Budgeting and proactive planning are associated with lower reported financial stress in several studies and reviews, though outcomes vary by person.

No overspending & goal achievement

Overspending becomes much harder because you've already allocated everything. When you want to buy something unplanned, you must consciously decide what to sacrifice. That friction (while sometimes annoying) protects you from impulse purchases that derail your goals.

Your financial goals get reached faster because you've built them into the budget. So if you want to save $5,000 for an emergency fund, you allocate money toward it every month, treating it like a bill that must be paid.

Waste elimination

Waste elimination happens naturally. According to research published in the Journal of Behavioral Decision Making, people naturally bucket money through mental accounting.

Zero-based budgeting leverages this by forcing explicit re-evaluation of each bucket, helping you spot subscriptions you forgot about and habits that drain your account.

The method works particularly well for irregular income. When you budget based on your minimum expected income, any extra becomes a bonus you can allocate strategically.

What are the challenges of zero-based budgeting?

Zero-based budgeting requires more effort than many other methods, especially initially. First of all, the time investment can feel overwhelming when you start. You'll spend several hours on your first budget, categorizing every expense and figuring out realistic amounts. Even after establishing your system, you'll need 30-60 minutes each month to plan and regular check-ins to track progress.

Harvard Business Review warns that zero-based budgeting "can work, but only with a huge amount of effort." Discipline and consistent tracking aren't negotiable. If you stop monitoring your spending mid-month, the whole system falls apart.

The method can feel restrictive when you're adjusting to it. Telling yourself "no" because a category is depleted stings, even when it's your own rule. Your first few months will include mistakes (forgetting categories, underestimating expenses, running out of money in important areas). You'll need patience while you figure out what works.

Who should use zero-based budgeting?

This method isn't universally perfect, but it excels in certain situations.

You'll thrive with zero-based budgeting if you appreciate detail and organization. People who enjoy tracking systems and having concrete data about their lives tend to love this approach.

Anyone working toward specific financial goals (paying off debt, saving for a house, building an emergency fund) benefits from the structure. Zero-based budgeting ensures your goals get funded every month because you've built them into the plan.

Variable income earners often find this method more helpful than percentage-based budgeting systems. When your income fluctuates, you need a flexible system that adjusts to what you actually earn.

Regular remittance senders can particularly benefit from planning transfers as a fixed expense. Instead of sending whatever is left over (which might be nothing some months), you budget your family support just like rent or utilities. However, the method might not suit you if you prefer simpler systems that require less maintenance. The best budget is the one you'll actually use.

How can you implement zero-based budgeting successfully?

Moving from concept to practice requires specific strategies that prevent common pitfalls.

Start with your actual income

Use real numbers, not optimistic projections. Check your last three months of bank statements to see what you actually earned after taxes. If you're expecting a raise, wait until that money hits your account before budgeting it.

For those sending money internationally, factor in that your usable income is your take-home pay. When planning transfers, account for the exchange rate. Some providers guarantee rates for a set window, while others book the rate at execution (RemitBee notes scheduled transfers are booked approximately 24 hours before execution), so check your provider's policy.

Choose the right tools

You don't need fancy software, but you do need some system for tracking:

- Paper and pencil (surprisingly effective)

- Budgeting apps (many sync with your bank)

- Spreadsheet templates (free and customizable)

- Envelope system (physical cash divided into categories)

The best tool is whichever you'll actually use consistently — a perfect system you abandon after two weeks is useless.

Plan for irregular expenses

Annual, quarterly, or occasional expenses wreck budgets when they surprise you. Car registration, insurance premiums, holiday gifts, and birthday celebrations all count.

Calculate the annual cost of each irregular expense, then divide by 12 to find the monthly amount. Set that money aside each month in a designated savings account or budget category. When the bill arrives, you've already got the money ready.

Read more about the Debt Snowball Method to build momentum and pay off your balances faster

Include a buffer category

Life happens, and rigid perfection is exhausting. Build in a small miscellaneous category (maybe $50-100) for truly unexpected expenses or minor category overruns — consider it as your budget insurance.

Review and refine monthly

Set aside time before each month begins to create next month's budget. Use what you learned from the current month to adjust categories that were too high or too low. Your spending patterns will shift seasonally (heating bills in winter, cooling costs in summer, holiday spending in December). Your budget should evolve with these changes rather than staying static all year.

Be realistic about spending categories

Underbudgeting creates a cycle of failure and frustration. If you actually spend $600 monthly on groceries for your family, don't budget $400 because it sounds better. You'll just overspend every month and feel defeated. So go ahead, and look at your last three months of actual spending to establish baseline amounts for variable categories. You can then decide if you want to reduce spending in certain areas, but start with reality.

What are common zero-based budgeting mistakes to avoid?

Even well-intentioned budgeters stumble over predictable obstacles.

Don’t be too restrictive

Being too restrictive backfires spectacularly. If you eliminate all fun spending to maximize debt payments or savings, you'll probably burn out within weeks. Include money for entertainment and personal enjoyment (even if it's a small amount). A sustainable budget beats a perfect budget you quit.

Don’t ignore irregular expenses

Forgetting annual or irregular expenses is the number one reason budgets implode mid-year. That $800 car insurance bill shouldn't be a surprise. Break it down into monthly chunks and set the money aside consistently.

Don’t stop tracking

Not tracking spending mid-month means flying blind. You might think you're doing fine with your grocery budget until you check at month-end and realize you overspent by $200 three weeks ago. Regular check-ins (even just weekly) keep you on track while there's still time to adjust.

Don’t ignore your life changes

Failing to adjust when life changes leads to abandoned budgets. If you got a raise, you must update your income and decide where the extra money goes. If you changed jobs with a longer commute, make sure to increase your transportation budget. If you moved to a cheaper apartment, reallocate that money intentionally.

How does zero-based budgeting help with international money transfers?

For many Canadians with family abroad, remittances are a significant monthly expense. Zero-based budgeting helps you handle transfers strategically rather than stressfully.

Planning remittances as a fixed expense means treating your family support like any other essential bill. You budget the amount you want to send each month, then protect that category the same way you protect your rent money. Your loved ones get consistent support, and you avoid the guilt of skipping months when money gets tight.

Accounting for exchange rates becomes easier when you're budgeting in advance. You can watch rates over several days and send when they're favorable (rather than rushing at the last minute). Services that provide rate visibility when you initiate the transfer give you budget certainty.

Making transfers fee-conscious fits naturally into zero-based budgeting's waste elimination mindset. When you're tracking every dollar, paying $25 in transfer fees that could be avoided feels unacceptable.

Building remittances into monthly allocations removes the emotional stress of deciding whether you can afford to send money. The decision is already made at the start of the month when you created your budget.

Transparent budgeting meets transparent remittances

Zero-based budgeting works because it eliminates surprises and puts you in control of every dollar you send to support family members. RemitBee brings that same transparency to your international money transfers, so you can budget with confidence knowing exactly what your family will receive.

- Multiple payment options (choose what fits your cash flow)

- Transparent FX margins shown upfront (no surprise deductions)

- Real-time exchange rate calculator (know exactly what you're sending)

- FINTRAC-registered MSB, and all transactions are fully insured

- $0 transfer fees on amounts of $500 CAD or more

Start your next international transfer with RemitBee and experience what transparent pricing really means.

Frequently asked questions

Here are some commonly asked questions about zero-based budgeting:

Can I use zero-based budgeting with irregular income?

Yes, though it requires adjusting your approach. Budget based on your lowest typical monthly income, then allocate any extra money when higher-earning months happen. You can assign the surplus to savings, debt, or sinking funds for leaner months. The key is staying conservative with your baseline expectations.

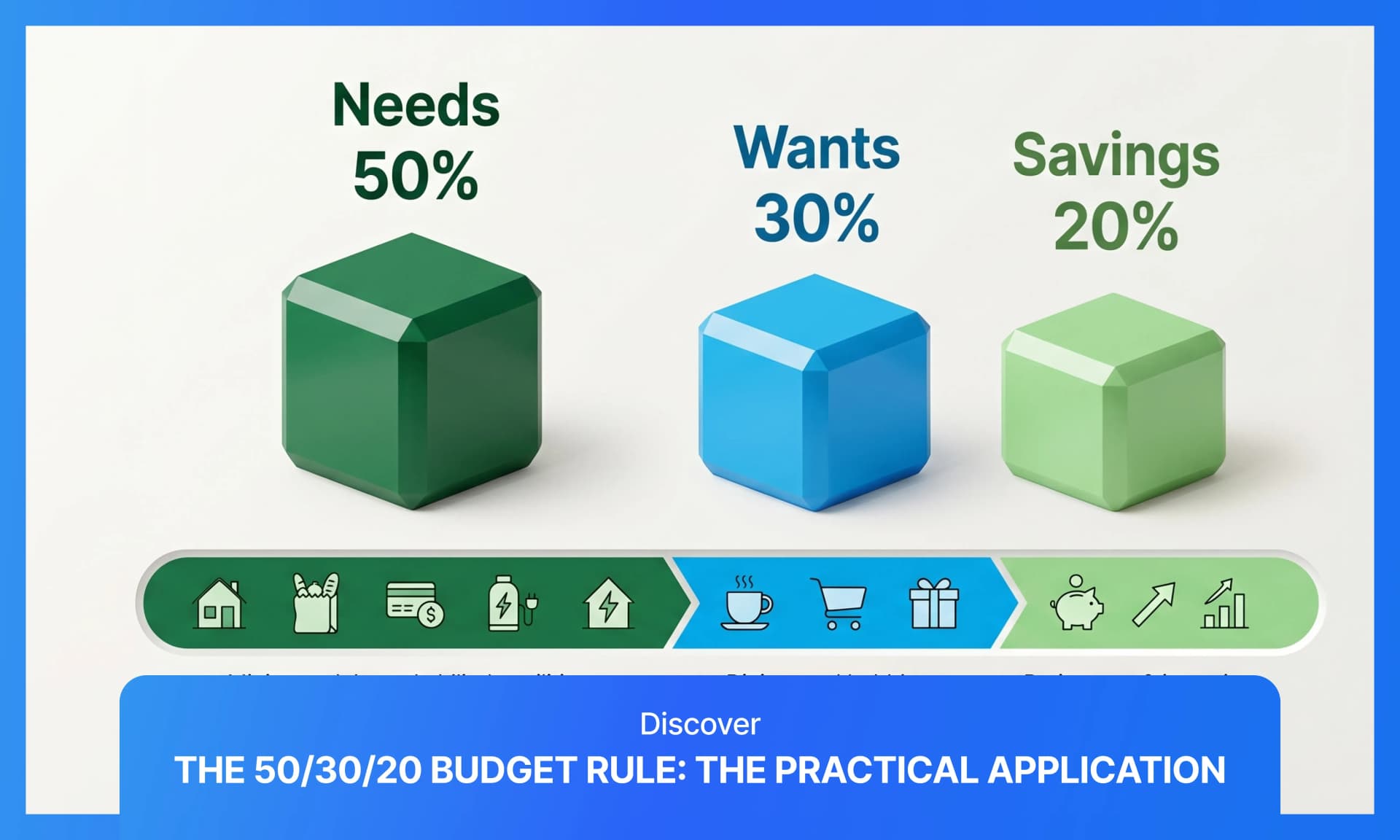

How is zero-based budgeting different from the 50/30/20 rule?

The 50/30/20 rule (popularized by Elizabeth Warren and Amelia Warren Tyagi in All Your Worth, 2005) divides income into percentages (50% needs, 30% wants, 20% savings) without tracking specific dollars. Zero-based budgeting accounts for every individual dollar and requires more detailed tracking. The 50/30/20 method is simpler; zero-based budgeting offers more control and precision.

What if I go over budget in a category?

You must pull money from another category to cover the overage. If you spent $50 more on groceries than planned, reduce your dining out budget, entertainment fund, or another flexible category by $50. This maintains the zero balance and forces you to make conscious trade-offs rather than just overspending.

How long does zero-based budgeting take each month?

Expect 2-3 hours for your first budget as you set up categories and estimate amounts. After that, monthly planning takes 30-60 minutes. You'll also need 5-10 minutes weekly to track spending and adjust categories. The time investment decreases as the process becomes routine.

Do I need to account for every single dollar?

Yes, but that doesn't mean tracking every penny with paranoid precision. Rounding to the nearest dollar is fine. The point is ensuring your entire income has an assignment, not creating accounting stress. If you're consistently within a few dollars of zero, your budget is working.

Can couples do zero-based budgeting together?

Absolutely, and many couples find it improves financial communication. Sit down together to create the budget, discuss priorities, and agree on category amounts. Regular budget meetings (weekly or monthly) keep both partners engaged and aware of the household's financial picture.

References

- Coyte, R., Gibbins, M., Li, B., & Thomas, D. (2022). The revival of zero-based budgeting: Drivers and consequences. Accounting & Finance, 62(3), 3717-3749.

- Government Accountability Office. (1979). Zero-base budgeting and sunset legislation: Congressional oversight responsibilities are not being fulfilled.

- Government Finance Officers Association. (n.d.). The bedrock of the budget process: Rethinking budgeting.

- Harvard Business Review. (2016). Zero-based budgeting is not a wonder diet for companies.

- McKinsey & Company. (2014). Five myths (and realities) about zero-based budgeting.

- McKinsey & Company. (2018). The return of zero-base budgeting.

- Nevada Legislative Counsel Bureau. (1979). Background Paper 79-6: Zero-based budgeting.

- Thaler, R. H. (1999). Mental accounting matters. Journal of Behavioral Decision Making, 12(3), 183-206.1099-0771(199909)12:3%3C183::AID-BDM318%3E3.0.CO;2-F)

- Thaler, R. H., & Benartzi, S. (2004). Save more tomorrow: Using behavioral economics to increase employee saving. Journal of Political Economy, 112(S1), S164-S187.

- Warren, E., & Warren Tyagi, A. (2005). All your worth: The ultimate lifetime money plan. Free Press.