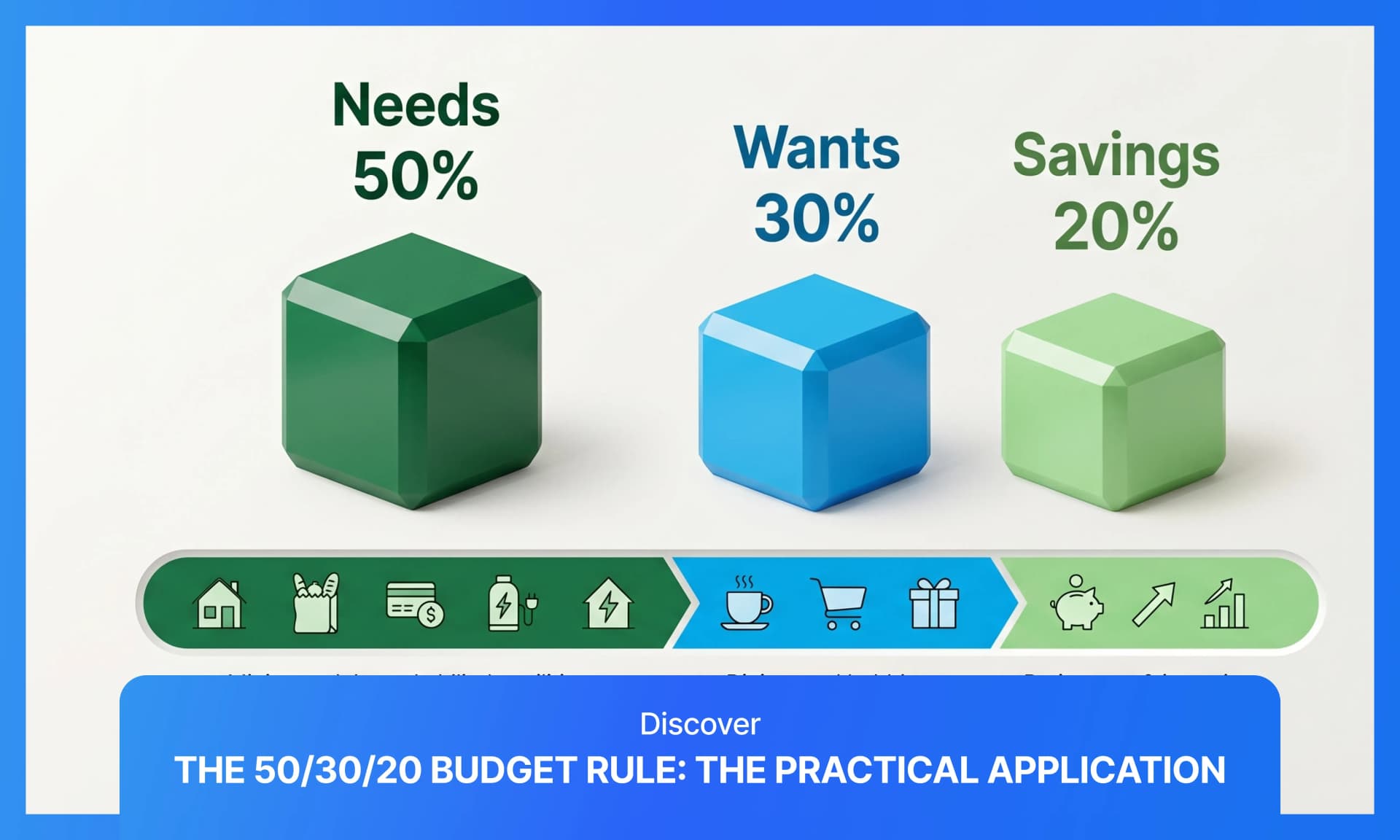

The 50/30/20 budget rule splits your after-tax income into three buckets:

- 50% for needs (rent, groceries, insurance, minimum debt payments)

- 30% for wants (dining out, subscriptions, travel)

- 20% for savings and extra debt repayment

Popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in All Your Worth, the framework gives you a big-picture financial structure without requiring you to track every coffee purchase.

The appeal is simplicity — three categories, one calculation, and no need for the mental gymnastics of spreadsheets full of complex formulae. In this read, we'll be exploring:

- How to implement the rule step by step

- Alternatives that work better in high-cost cities

- How to calculate your after-tax income correctly

- Why the 20% savings bucket is the most underrated part

- What to do when your rent alone eats 40% of your income

- What qualifies as a need vs. a want (and where people draw the line wrong)

TLDR: The 50/30/20 Rule at a Glance

Here is a quick summary before the full breakdown.

| Bucket | % of After-Tax Income | What It Covers |

|---|---|---|

| Needs | 50% | Rent/mortgage, utilities, groceries, transportation, insurance, minimum debt payments |

| Wants | 30% | Dining out, entertainment, travel, subscriptions, non-essential shopping |

| Savings & Debt | 20% | Emergency fund, retirement, investments, extra debt payments |

How Do You Calculate Your Starting Number?

The entire rule runs on after-tax income — the amount that hits your bank account after federal, provincial, and mandatory deductions. For salaried employees, the net pay on your stub is the baseline.

The tricky part is that if your employer auto-deducts retirement contributions or health insurance, some financial advisors recommend adding those back in before applying the 50/30/20 split. The logic is that those deductions are part of your budget — retirement contributions belong in the 20% savings bucket, and health insurance is a "need." Ignoring them skews the percentages.

For freelancers and self-employed Canadians, calculate after-tax income by subtracting estimated taxes and business expenses from gross revenue. A budgeting app that connects to your accounts can automate the tracking.

What Counts as a Need vs. a Want?

The distinction sounds obvious until you try to categorize your actual spending. The test is: would skipping this payment create serious consequences (eviction, legal trouble, job loss, illness)? If yes, it is a need. If no, it is a want.

Needs (50%)

Expenses that keep you alive, employed, and legally compliant:

- Groceries (not restaurants)

- Rent or mortgage payments

- Minimum required payments on all debts

- Insurance premiums (health, auto, home)

- Basic utilities (electricity, water, heat, phone)

- Transportation to work (car payment, gas, transit pass)

Wants (30%)

Discretionary spending on things you enjoy but could survive without:

- Streaming services and gym memberships

- Non-essential clothing and electronics

- Hobbies and entertainment

- Restaurants and takeout

- Travel and vacations

The boundary gets blurry. A basic phone plan is a need; a premium unlimited plan is partially a want. Basic groceries are a need, while organic specialty items inch toward a want. Be strict with yourself — lifestyle creep inflates the "needs" category faster than anything else.

Savings and Debt (20%)

The bucket that builds your future:

- Retirement contributions (RRSP, TFSA)

- Investments and long-term savings goals

- Emergency fund (3–6 months of expenses)

- Extra debt repayment (above the minimum)

Minimum debt payments go under "needs." Only extra payments toward principal count as savings.

How Do You Implement It Step by Step?

The implementation is straightforward once you know your numbers.

- Calculate your monthly after-tax income

- Pull 1–3 months of bank and credit card statements

- Categorize every expense into needs, wants, or savings

- Compare your actual split to 50/30/20

- Trim wants first if needs exceed 50%

- Automate the 20% savings transfer on payday (before you spend it)

If your current split is 65/25/10, you are not "failing" — you have a target to work toward. The rule is a guideline, not a law. Gradual progress (moving from 10% savings to 15%, then 20%) is more sustainable than overnight austerity.

What If the 50% for Needs Is Not Realistic?

In expensive cities like Vancouver, Toronto, or Calgary, rent alone can consume 35–45% of after-tax income. Hitting the 50% cap for all needs feels impossible — and for many Canadians, it is (at least temporarily).

The adjustments that work:

- Trim wants to 20% and redirect the 10% to cover excess needs

- Consider proportional variations like 60/20/20 or 70/15/15

- Reduce fixed costs (roommate, cheaper neighbourhood, public transit)

- Increase income through side work or career progression

The 50/30/20 works best as an aspiration in high-cost markets, not as a rigid constraint. The one number to protect above all else is the savings rate — even a 10% savings rate, automated on payday, compounds into real wealth over time. For Canadians budgeting while supporting family abroad, the wants category is typically where the squeeze happens.

What Are the Main Alternatives?

Several variations exist for different financial situations:

| Rule | Split | Best For |

|---|---|---|

| 80/20 | 80% spend, 20% save | People who hate categorizing |

| 70/20/10 | 70% needs+wants, 20% savings, 10% debt/giving | High-cost cities |

| 60/30/10 | 60% needs, 30% wants, 10% savings | Temporary high-expense phases |

| Zero-based | Every dollar is assigned a "job" | Detail-oriented budgeters |

| Reverse budgeting | Save first, spend whatever remains | Aggressive savers |

Zero-based budgeting assigns every dollar to a purpose before the month begins. Reverse budgeting automates savings upfront and spends the rest without guilt. Both can work alongside or replace the 50/30/20, depending on your discipline level and financial goals.

Build Your Budget — and Protect Your Family Transfers

Whether you follow the 50/30/20 rule or a variation of it, sending money home should not destroy your budget. RemitBee keeps transfer costs low.

- Best exchange rates in Canada

- FINTRAC-regulated, fully compliant

- Zero fees on transfers over $500 CAD

- 100% money back guarantee on all transfers

Frequently Asked Questions

Is the 50/30/20 Rule Based on Gross or Net Income?

The 50/30/20 rule is based on net income, meaning after-tax income or take-home pay. It is meant to divide the money you can actually spend, save, or use to repay debt. Some budget calculators add back payroll deductions for workplace retirement contributions, health insurance, or automatic savings before applying the split, since those amounts already belong in the savings or needs categories. The main point is consistency: use the same income base each month, then divide it into 50% needs, 30% wants, and 20% savings or debt repayment.

Where Do Minimum Debt Payments Fall in the 50/30/20 Rule?

Minimum required debt payments usually fall under the 50% needs category because they are obligations, not optional choices. This includes minimum payments on credit cards, student loans, car loans, personal loans, and similar debts. Missing them can lead to late fees, credit damage, collection action, or legal consequences. Extra payments above the required minimum are treated differently — those extra amounts usually belong in the 20% savings and debt repayment category, because they are part of your plan to build net worth and reduce future interest costs faster.

What If I Can Only Save 10% Right Now?

Start with 10% and make it automatic. The 50/30/20 rule is a guide, not a pass-or-fail test, and a smaller savings habit that actually happens is better than a 20% goal that never gets funded. Set the transfer for payday so the money leaves before casual spending begins. Then raise the rate by 1% or 2% when income rises, a bill disappears, or you trim a recurring cost. Keeping the habit steady matters most, especially while you build a starter emergency fund and avoid relying on debt.

Should I Use the 50/30/20 Rule If I Have High-Interest Debt?

Yes, but modify it while the debt is expensive. The standard rule puts 30% toward wants and 20% toward savings and debt repayment, but high-interest credit card debt can grow quickly if only minimums are paid. A temporary version, such as 50/10/40, can make sense: cover needs, keep wants modest, and push more cash toward debt repayment plus basic savings. Keep at least a small emergency cushion so one surprise cost does not send you back to credit cards. Once high-interest debt is gone, return to a more balanced 50/30/20 split.