The median net worth of Canadian families was $519,700 in 2023, according to Statistics Canada's Survey of Financial Security — the most recent detailed household wealth survey available.

Since then, overall Canadian household wealth has continued rising, with total household net worth reaching $18.6 trillion by the end of 2025.

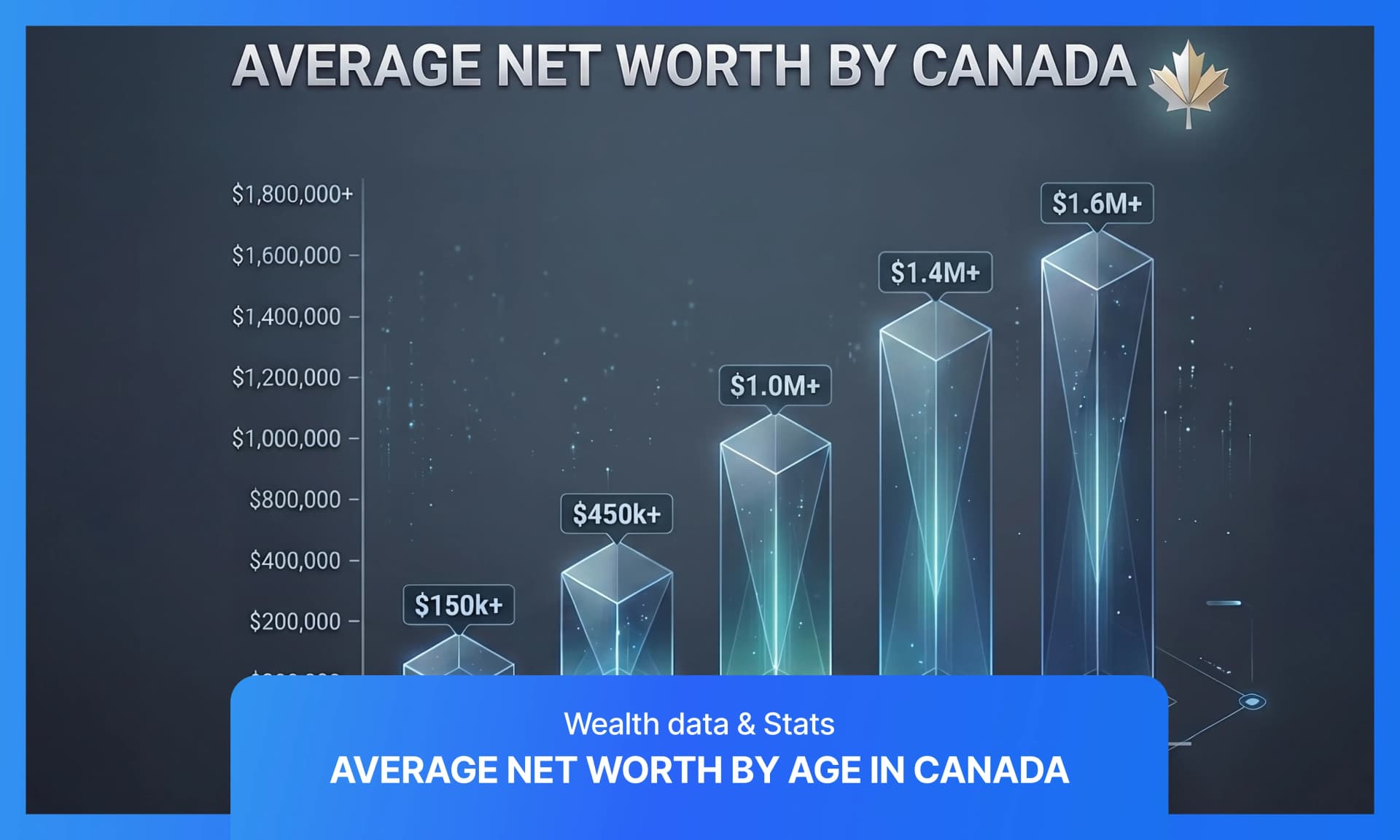

Net worth — total assets minus debts — follows a life-cycle curve, climbing through working years, peaking between ages 55 and 64 at $873,400, and declining after retirement begins.

However, the age-based curve hides sharper divides driven by homeownership, pension access, immigration timeline, and asset mix.

Median figures are far more reliable than averages here, because the top 20% of Canadian families hold nearly two-thirds of all household wealth.

The research below covers:

- 2025 updates showing $18.6 trillion in total household wealth

- Median and average net worth benchmarks for every age group

- Wealth patterns among immigrant versus Canadian-born households

- How pension access and home equity create a $1.4 million gap before retirement

- Debt-to-income ratios by age and the mortgage renewal risk ahead

- Why the "average" number overstates what most families have

- The homeownership split within younger households

What Is the Median Net Worth by Age in Canada?

Statistics Canada's 2023 Survey of Financial Security remains the most recent age-disaggregated snapshot of Canadian household wealth. The table below shows median net worth by the age of the household's major income earner.

| Age of the Major Income Earner | Median Net Worth (2023) |

|---|---|

| Under 35 | $159,100 |

| 35 to 44 | $409,300 |

| 45 to 54 | $675,800 |

| 55 to 64 | $873,400 |

| 65 and older | $738,900 |

| All Canadian families | $519,700 |

Accumulation Phase

Wealth builds through the prime earning decades as households gain home equity, contribute to retirement accounts, and pay down debt. The peak sits in the 55-to-64 bracket, just before or at the start of retirement.

Drawdown Phase

After 65, median net worth drops as families begin spending their RRSPs, converting savings to income (RRIFs), selling investments, or downsizing homes. The decline is expected — it reflects the purpose of saving, which is to eventually use the savings.

Hidden Variation

The curve masks enormous differences within each age group. A 30-year-old homeowner in Calgary and a 30-year-old renter in Toronto may sit in the same bracket but occupy entirely different financial positions. Age is the starting point for comparison, not the full picture.

Why Does the Average Net Worth Number Mislead Most Canadians?

The average (mean) net worth of Canadian families in 2023 was approximately $738,200, according to Statistics Canada — nearly $220,000 higher than the median. That gap alone signals a problem with using averages as a personal benchmark.

Wealth Concentration

The Parliamentary Budget Officer quantified the skew in a 2025 update.

| Wealth Group | Share of Total Net Wealth (2023) |

|---|---|

| Top 1% | 23.8% |

| Top 10% | 53.0% |

| Top 20% | 69.0% |

The PBO also estimated that approximately 4.4 million Canadian families had net wealth above $1 million, while about 108,000 families exceeded $10 million.

Survey Limitations

Statistics Canada itself notes that the Survey of Financial Security does not fully capture the wealthiest households, meaning even the PBO's top-tail estimates are conservative.

When a single billionaire household can pull up the average by a measurable amount, the mean becomes a misleading yardstick.

Practical Takeaway

For any self-assessment, median net worth is the right comparison. It describes the family sitting right in the middle of the distribution, not the one distorted by extreme outliers at the top.

What Splits Younger Households Into Wealth Winners and Losers?

Families where the major income earner was under 35 recorded a 179% increase in real median net worth between 2019 and 2023, reaching $159,100.

That sounds like a dramatic improvement — but the percentage gains started from a low base, and the growth was not evenly distributed.

Homeownership Divide

Statistics Canada broke the under-35 group into homeowners and non-homeowners, and the split is stark.

| Under-35 Families | Median Net Worth (2023) |

|---|---|

| Own their principal residence | $457,100 |

| Do not own their principal residence | $44,000 |

Young homeowners reached $457,100 in median net worth, boosted by $142,800 in gains since 2019 (driven primarily by rising home values). Young renters sat at $44,000. The gap between the two groups — more than $400,000 — is wider than the median net worth of the entire under-35 cohort.

Generational Shift

A Statistics Canada study published in May 2026 confirmed the scale of the change.

After adjusting for the growing share of young adults still living with parents, millennials recorded an adjusted homeownership rate of 49.9% — below the 56.2% rate Gen-Xers had at the same age and the 55.9% rate baby boomers recorded in 1991.

Census data shows the steepest drops among the youngest buyers:

- Age 25–29 homeownership fell from 44.1% (2011) to 36.5% (2021)

- Age 30–34 homeownership fell from 59.2% to 52.3%

Compounding Cost

For younger Canadians trying to build credit and save toward homeownership, the challenge is that the asset responsible for most wealth-building — real estate — has become harder to access at the exact life stage when entering the market would produce the longest compounding period. Missing that window has consequences that echo across every decade that follows.

Where Does the Real Wealth Gap Open Before Retirement?

The most powerful finding in the 2023 Survey of Financial Security is not the age-based curve. It is what happens when homeownership and pension access are layered on top of age.

Four Realities

Among families where the major income earner was 55 to 64, Statistics Canada reported four distinct financial positions.

| 55-to-64 Families | Median Net Worth (2023) |

|---|---|

| Own home + employer pension | $1,400,000 |

| Own home, no employer pension | $914,000 |

| Employer pension, no home | $359,000 |

| No home, no employer pension | $11,900 |

Home Equity Dominance

The distance between the top and bottom rows is staggering — $1.4 million versus $11,900. Home equity is the larger contributor to that gap. The $914,000 figure for homeowners without a pension versus $359,000 for pension holders without a home confirms this.

Pension Access

Pension coverage adds a meaningful second layer. Workers in the public sector, unionized environments, or larger employers with defined benefit plans accumulate a retirement asset that compounds quietly for decades. Workers in gig roles, small businesses, or contract-based arrangements never build that layer at all.

Practical Implication

Two Canadians can earn similar incomes across a 30-year career and still arrive at retirement with a $1.3 million difference in wealth, depending almost entirely on whether they had access to affordable housing and an employer-backed pension.

For Canadians thinking about how to invest in stocks or build an emergency fund, the data makes the priority clear — if homeownership is financially viable, it remains the single most effective wealth-building tool for most households.

How Heavy Is the Debt Burden Across Age Groups?

Net worth is a snapshot of assets minus debts, but it does not reveal monthly cash-flow pressure. A family with $500,000 in home equity and $450,000 in outstanding mortgage debt has positive net worth, but tight monthly breathing room — especially if payments are about to rise.

Debt-to-Income Ratios

Statistics Canada's Q4 2025 household accounts data reported ratios by age.

| Age Group | Debt-to-Income Ratio (Q4 2025) |

|---|---|

| Under 35 | 166.0% |

| 35 to 44 | 245.8% |

The 35-to-44 group carries the heaviest load at 245.8%, reflecting peak mortgage balances, childcare costs, and early-career earnings that haven't caught up to the obligations built during the housing entry phase.

Mortgage Renewals

The Bank of Canada estimated that about 60% of mortgage holders renewing in 2025 and 2026 would see payment increases:

- Average payments could be 10% higher for 2025 renewals

- Average payments could be 6% higher for 2026 renewals

- Five-year fixed borrowers could face 15% to 20% increases

Stress Test Buffer

The Bank of Canada's Financial Stability Report (May 2025) offered some balance — more than 90% of mortgage holders with five-year fixed rates would face increases smaller than what they were stress-tested for.

Most borrowers should absorb the higher payments, but "should" and "will" are different words when groceries, childcare, and credit card debt are competing for the same paycheque.

What Does a Typical Canadian Family Balance Sheet Look Like?

The net worth number is a single figure, but the composition tells you where risk and opportunity sit. Statistics Canada's 2023 infographic breaks down the most common categories.

Asset Side

| Asset Type | Median Value (2023) |

|---|---|

| Principal residence | $500,000 |

| Retirement assets | $161,800 |

| Vehicles | $20,000 |

| Bank deposits and financial assets | $26,000 |

Debt Side

| Debt Type | Median Value (2023) |

|---|---|

| Mortgage on principal residence | $200,000 |

| Vehicle loans | $20,000 |

| Student loans | $14,000 |

| Lines of credit, cards, instalment debt | $9,000 |

Composition

For most families, net worth is overwhelmingly a home equity story.

The principal residence at $500,000 minus the mortgage at $200,000 produces $300,000 in home equity alone — the majority of total wealth for many households. Retirement assets at $161,800 form the second pillar. Everything else is comparatively small.

For renters, the balance sheet looks fundamentally different. Without a principal residence, wealth accumulation depends almost entirely on retirement accounts and savings — categories where the median values ($26,000 in deposits and financial assets) would not last long during an extended job loss or emergency.

How Do Immigrant Families Compare on the Wealth Curve?

Immigration status adds a distinct dimension to the net worth picture. For RemitBee's audience — many of whom are newcomers, immigrants, or families with cross-border financial obligations — the data is both encouraging and sobering.

Recent Immigrants

A March 2026 Statistics Canada study found that recent immigrant families aged 25 to 44 had a median net worth of $132,300 — less than half the $293,900 for Canadian-born families in the same age range.

| Family Type (Age 25 to 44) | Median Net Worth (2023) |

|---|---|

| Recent immigrants | $132,300 |

| Canadian-born | $293,900 |

| Gap | $161,600 |

The gap reflects delayed housing market entry, fewer years in employer pension systems, and the cost of settlement itself.

Recent immigrants had lower average principal residence equity ($145,700 versus $194,600) and significantly weaker pension positions — RPP assets accounted for just 7% of wealth, compared with 15% for Canadian-born families.

Established Immigrants

The picture reverses with time. Established immigrant families aged 35 to 64 had median net worth of $751,500, surpassing the $608,400 figure for comparable Canadian-born families.

| Family Type (Age 35 to 64) | Median Net Worth (2023) |

|---|---|

| Established immigrants | $751,500 |

| Canadian-born | $608,400 |

Convergence Pattern

The convergence and eventual overtaking suggests that immigrant wealth accumulation in Canada is strongly time-sensitive — early disadvantage gives way to above-average outcomes given sufficient tenure in the housing and labour markets.

For newcomers building financial literacy, the early years are financially the hardest, but the long-term trajectory is strong for those who gain access to homeownership and stable employment.

The open question is whether today's housing market allows the same catch-up pattern that earlier immigrant cohorts achieved.

Did Household Wealth Keep Growing After 2023?

The Survey of Financial Security captures a snapshot, but household wealth is not frozen at the 2023 figures.

Statistics Canada's national balance sheet data shows that total Canadian household net worth reached $18.6 trillion by Q4 2025, after adding more than $1 trillion during the year.

Growth Drivers

| National Wealth Metric (Q4 2025) | Value |

|---|---|

| Total household net worth | $18.6 trillion |

| Quarterly increase | +$230.2 billion |

| Annual financial asset growth | +10.5% |

| Annual real estate change | −0.7% |

| Annual mortgage debt growth | +4.2% |

Financial assets rose 10.5% year over year, while real estate values dipped 0.7%. Since equities, mutual funds, and pension balances are concentrated among wealthier and older households, the 2025 growth was not neutral across demographics.

Uneven Distribution

Statistics Canada's distributional data confirmed the lopsided outcome:

- Top 20% held 65.7% of total net worth, averaging $3.5 million per household

- Bottom 40% held just 3.0%, averaging $81,650 per household

- Under-35 households grew average wealth by 5.7%, but mortgage debt also rose 3.7%

Widening Gap

The income gap also widened in 2025. Lower-income households were hit by declining interest rates (reducing returns on savings) and weak employment income growth, while wealthier households rode the continued strength in equity markets. Wealth growth, in other words, went where wealth already existed.

What Does Net Worth Miss About Financial Well-Being?

A positive net worth figure does not mean a household is financially secure. Two data points illustrate the gap between balance-sheet wealth and lived experience.

Literacy vs. Security

The Financial Consumer Agency of Canada reported that while 72.5% of Canadians demonstrated positive financial knowledge by March 2025, only 56.7% demonstrated good financial well-being — falling short of FCAC's own 60% target.

Knowing how to manage money and actually feeling stable are not the same thing, particularly when housing costs, debt service, and inflation eat into disposable income regardless of what the net worth line says.

Insolvency Reality

The Office of the Superintendent of Bankruptcy reported that consumer debtors in 2024 had median total assets of just $15,142 against median total liabilities of $53,997 — a negative net difference of $38,855.

| Metric | General Population (2023) | Consumer Debtors (2024) |

|---|---|---|

| Median total assets | $680,200 | $15,142 |

| Median total debts | $100,000 | $53,997 |

| Median net worth | $519,700 | −$38,855 |

Beyond the Number

The contrast reinforces a broader theme — headline net worth benchmarks are useful for orientation but dangerous for complacency.

A household can look "normal" on the age curve while carrying deeply fragile finances underneath, especially if most of the net worth is locked in a home that cannot be easily liquidated.

For anyone assessing their own position, the better exercise is not just comparing net worth to the age benchmark. Ask whether the household can absorb a $500 surprise expense, whether it has three to six months of emergency savings, and whether debt service leaves room to save consistently.

If the answer to any of those is no, the net worth figure is a ceiling, not a floor.

Frequently Asked Questions

How Is Net Worth Calculated?

Net worth equals total assets minus total liabilities. Assets include principal residence value, retirement accounts (RRSPs, TFSAs, employer pensions), vehicles, bank deposits, and investments. Liabilities include mortgages, vehicle loans, student debt, credit card balances, and lines of credit. For most Canadian families, the principal residence is the largest asset and the mortgage is the largest liability.

What Is a Good Net Worth for a 30-Year-Old in Canada?

The median net worth for all under-35 families was $159,100 in 2023. However, that includes homeowners ($457,100 median) and non-homeowners ($44,000 median). A 30-year-old renter with $50,000 or more in net worth is performing at or above median for their tenure type. A 30-year-old homeowner would need roughly $400,000 or more to sit near the median for young homeowning families.

Why Does Net Worth Drop After Age 65?

Median net worth peaks in the 55-to-64 bracket ($873,400) and declines to $738,900 for families 65 and older because retirement triggers a drawdown phase. Families begin spending RRSPs, converting savings to income (RRIFs), selling investments, or downsizing. The decline does not necessarily signal financial distress.

Do Immigrants in Canada Have Lower Net Worth?

Recent immigrants do, but established immigrants do not. Recent immigrant families aged 25 to 44 had median net worth of $132,300 in 2023 — less than half the $293,900 for Canadian-born families. However, established immigrant families aged 35 to 64 had median net worth of $751,500, surpassing the $608,400 for comparable Canadian-born families. The gap closes with time, driven by homeownership access, pension accumulation, and income growth.

How Much Debt Is Normal for a 35-to-44-Year-Old?

The 35-to-44 age group carries the highest debt-to-income ratio at 245.8% as of Q4 2025 (Statistics Canada). For every dollar of disposable income, the average household owes about $2.46 in debt — mostly mortgage-related, coinciding with peak homebuying activity and family formation costs. The ratio typically declines through the 45-to-54 and 55-to-64 brackets as mortgages are paid down.

References

- Statistics Canada. "Survey of Financial Security, 2023." October 29, 2024.

- Office of the Parliamentary Budget Officer. "Estimating the top tail of the family wealth distribution in Canada: 2025 update." September 11, 2025.

- Statistics Canada. "National balance sheet and financial flow accounts, fourth quarter 2025." March 16, 2026.

- Statistics Canada. "Distributions of household economic accounts, fourth quarter 2025." April 13, 2026.

- Bank of Canada. "How will mortgage payments change at renewal? An updated analysis." July 2025.

- Bank of Canada. "Financial Stability Report, 2025." May 2025.

- Statistics Canada. "Trends in the wealth gap between immigrant and Canadian-born families from 2016 to 2023." March 25, 2026.

- Statistics Canada. "Millennials in the Canadian housing market: An intergenerational comparison." May 2026.

- Statistics Canada. "The assets, debts and net worth of Canadian families, 2023." October 29, 2024.

- Office of the Superintendent of Bankruptcy. "Canadian Consumer Debtor Profile, 2024." November 27, 2025.

- Financial Consumer Agency of Canada. "Annual Report 2024 to 2025." October 20, 2025.